When the FOMC ultimately decides that short-term nominal interest rates in U.S. financial markets should rise, a lot will have changed since pre-financial crisis times. Principally, the Fed's balance sheet is about 5 times larger, total reserves have increased from about $10 billion on average in 2007 to about $2.8 trillion currently, and the Fed now pays interest on reserves.

Any central bank with a significant quantity of excess reserves outstanding overnight operates within a floor system, in which the interest rate on overnight liabilities of the central bank determines the overnight interest rate - in a financial system with no significant frictions. In the case of the U.S. Federal Reserve System, the frictions make all the difference, and create a thorny monetary policy problem for liftoff from essentially-zero overnight nominal interest rates.

The Fed's problem would be easy in a financial system like that in Canada, for example. In normal times, the Bank of Canada operates under a channel system. It targets an overnight interest rate, which is subject to an upper bound, which is the rate at which the Bank lends to financial institutions (the "Bank rate"), and a lower bound, which is the deposit rate for financial institutions at the Bank - the counterpart of the interest rate on reserves, or IOER in the U.S. Typically, the Bank rate is set at 0.25% above the target, and the deposit rate at 0.25% below the target. The idea is that no financial institution would borrow from another one at a rate above the Bank rate, nor would it lend to another financial institution at a rate below the Bank's deposit rate, so arbitrage will keep the target rate between the upper and lower bounds. Here's a chart showing the actual overnight rate in Canada:

Though normally the Bank of Canada operates a channel system, from April 21, 2009, to June 1, 2010, there was a floor system in Canada. Over this period, the Bank's deposit rate and the target rate were both set at 0.25%, with the Bank rate at 0.50%. Commensurate with that configuration of policy rates, the Bank also kept a positive quantity of reserves in the financial system overnight:

But, you might say, that's not what has been happening in the United States since the financial crisis. There is a very large quantity of excess reserves in the U.S. financial system, and the IOER has been set at 0.25% since late 2008, but the fed funds rate - the overnight rate the FOMC currently focuses on - looks like this:

When Congress amended the Federal Reserve Act to permit payment of interest on reserves by the Fed, it specified that government-sponsored enterprises (GSEs) could not receive these payments. The key GSEs that matter in this respect are Fannie Mae, Freddie Mac, and the Federal Home Loan Banks (FHLBs). Most people know what Fannie Mae and Freddie Mac are up to, but most economists I have run into had no idea until recently what a FHLB is. The FHLB system was set up during the Great Depression as a housing finance vehicle. There are twelve FHLBs, each with a district (much like Fed districts, though FHLB districts are not identical to Federal Reserve districts) and member financial institutions. The members each hold nontradeable stock in the FHLB, and the primary activity of a FHLB is issuing tradeable securities to finance lending to member institutions. This lending is typically secured by mortgages, and the intention seems to be to direct financing toward low-income mortgage borrowers. FHLBs also hold a relatively small portfolio of mortgages, purchased outright. As is the case with Fannie Mae and Freddie Mac, FHLBs have reserve accounts with the Fed and, since GSEs receive zero interest on those reserve balances while commercial banks and other financial institutions currently receive interest at the current IOER rate of 0.25%, there would appear to be gains from trade.

GSEs which would otherwise hold reserve balances overnight could lend overnight on the fed funds market to commercial banks, for example. Those commercial banks could then hold the funds as reserves overnight, earning 0.25%, pay the GSEs x%, where 0 < x < 0.25, make a profit, and the GSEs and commercial banks would be better off as a result. Indeed, frictionless arbitrage would dictate that the GSEs would get all of the gains from trade, with x = 0.25. Why is this arbitrage activity, between GSEs and financial institutions with interest-bearing reserves important? Given that the U.S. financial system is awash in reserves, we might predict that there would be little reason for any financial institution to borrow on the fed funds market overnight, so that most fed funds activity should currently just be arbitrage. Indeed, Afonso et al. estimate that about 75% of lending on the fed funds market was accounted for by FHLBs, by the end of 2012.

But why is the arbitrage not perfect, or even close to it? Financial institutions that receive interest on reserves also face balance sheet costs associated with borrowing on the fed funds market. For example, deposit insurance premia depend on total assets, and there are capital requirements and other restrictions on commercial banks. As a result, the cost of fed funds borrowing is idiosyncratic - it will depend on a bank's size, and on the composition of its portfolio, for example. Of particular note is that branches of foreign banks in the U.S., because they do not have domestic retail deposits, do not pay deposit insurance premia, so they have a cost advantage over domestic banks in borrowing on the fed funds market. What would we predict then? Branches of foreign banks should be borrowing fed funds from FHLBs. Again, Afonso et al. estimate that, by the end of 2012, about 60% of borrowing on the fed funds market was being done by foreign-owned banks.

Liftoff?

Once liftoff occurs, presumably with a stock of reserves in the financial system that is on the order of what it is currently, what would happen if the Fed adhered to its existing operating strategy? One might expect that, as the IOER increased, the fed funds rate would follow. Perhaps the current margin of about 15 basis points between the IOER and the fed funds rate would be maintained. Perhaps that margin would increase. It's hard to say, given our imperfect understanding of what explains the margin in the first place. One might also ask: who cares about the margin anyway? Surely the overnight rate that is critical to most financial market participants is the IOER? Maybe in this idiosyncratic floor system we should be ignoring fed funds market activity, as that is just about arbitrage between GSEs and foreign-owned banks?

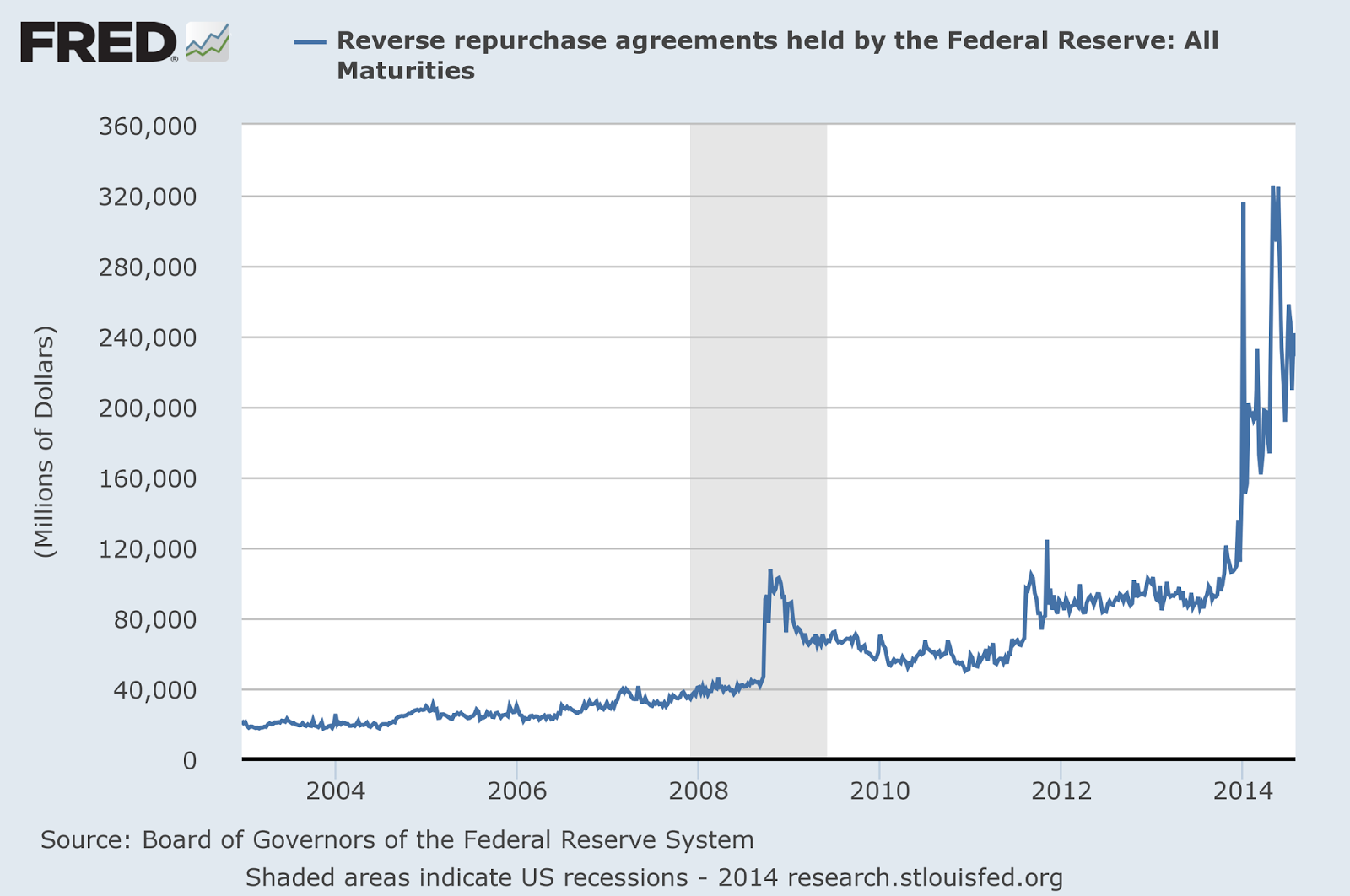

There are other alternatives, though. The New York Fed has been conducting experiments using an overnight reverse repurchase agreement (or ON RRP) facility. A reverse repo for the Fed consists of a loan, typically overnight, to the Fed, secured by collateral (typically Treasury securities) from the Fed's asset portfolio. But why would the Fed need to post collateral on a loan? Surely the Fed is good for it? But, if the Fed were to borrow unsecured, we would call that reserves. If the Fed borrows by way of reverse repos, then it is permitted to pay interest to anyone, including GSEs, and it can also borrow from financial institutions that do not hold reserve accounts. Indeed, to enlarge the set of financial institutions that can hold interest-bearing Fed liabilities, the New York Fed has approved an expanded list of counterparties which includes domestic commercial banks, foreign-owned banks, GSEs (including some FHLBs) and money market mutual funds (which do not have reserve accounts). ON RRP activity by the Fed is shown in the next chart:

But, given that the ON RRP facility now exists, what to do with it? To figure this out, it helps to understand how policy would work in the liftoff phase in the absence of ON RRPs. Given the size of the Fed's portfolio, total liabilities of the Fed - in this case currency and reserves - is essentially fixed in nominal terms. For a particular IOER, asset prices, the prices of goods and services, and quantities, including the fraction of Fed liabilities held as reserves, adjust so that consumers and financial institutions are willing to hold the total stock of Fed liabilities. If the Fed sets a higher IOER, then everything adjusts, and presumably the fraction of Fed liabilities consisting of reserves will increase.

Now, throw ON RRPs into the mix. There are different ways in which the Fed could intervene in the repo market. For example, the Fed could decide on a quantity of borrowing on a particular day, and then conduct an auction among its counterparties. However, what the Fed seems to ultimately envision is a "fixed rate, full allotment" allocation mechanism, according to which a rate is set, and the fed accepts whatever is forthcoming at that rate. So far, full allotment appears not to have been attempted, as the ON RRP experiments conducted by the New York Fed, beginning in January of this year involved putting per-counterparty caps on takeup, with a fixed rate of .05%. Caps were increased over time, to $10 billion per counterparty in April 2014. As you can see in the last chart, outstanding ON RRPs in the last few months have come in mostly between $200 billion and $300 billion - on average somewhat less than 10% of total interest-bearing Fed liabilities.

Given a setting for IOER, there will in general be some critical value for the spread between the IOER and the ON RRP rate such that takeup is zero below that rate, and positive above it. From the New York Fed's experiments, it seems we are safe in assuming that this critical spread is at least 20 basis points. Further, suppose the spread is lower than the critical value, and the ON RRP rate increases with IOER held fixed. What happens? Fed liabilities will in general be more attractive, and ON RRPs will be more attractive relative to either reserves or currency. We would expect that short-term market interest rates would increase (not IOER of course), and more Fed liabilities would be held in the form of ON RRPs, with less held as reserves and currency. For example, perhaps some FHLBs which would formerly have been lenders on the fed funds market would now hold ON RRPs. This would reduce reserves and activity on the fed funds market.

Clearly, given the IOER, the ON RRP rate can be sufficiently high that reserves go to zero. That is, we know that if the ON RRP rate exceeds IOER, then no financial institution would wish to hold reserves. But, it's possible that reserves could go to zero with the ON RRP rate less than IOER, if there is sufficient demand for ON RRPs from the GSEs and money market funds. Further, with sufficient interest-bearing Fed liabilities in the system, it is possible that the ON RRP rate could be high enough that fed funds market activity could dwindle essentially to zero. We know that much of current fed funds market activity is just the result of arbitrage between GSEs and banks that earn interest on reserves, and this arbitrage activity would go away with a sufficiently high ON RRP rate.

Concerns

So, now that we have thought through how a system with three primary Fed liabilities - currency, reserves, ON RRPs - might work, what potential concerns might there be with such a framework?

1. There is potentially a lot going on here. How will the FOMC communicate monetary policy actions to the public in a simple and clear fashion? This was one of the subjects of discussion at June FOMC meeting (see the minutes):

Most participants agreed that adjustments in the rate of interest on excess reserves (IOER) should play a central role during the normalization process. It was generally agreed that an ON RRP facility with an interest rate set below the IOER rate could play a useful supporting role by helping to firm the floor under money market interest rates. One participant thought that the ON RRP rate would be the more effective policy tool during normalization in light of the wider variety of counterparties eligible to participate in ON RRP operations. The appropriate size of the spread between the IOER and ON RRP rates was discussed, with many participants judging that a relatively wide spread--perhaps near or above the current level of 20 basis points--would support trading in the federal funds market and provide adequate control over market interest rates. Several participants noted that the spread might be adjusted during the normalization process. A couple of participants suggested that adequate control of short-term rates might be accomplished with a very wide spread or even without an ON RRP facility. A few participants commented that the Committee should also be prepared to use its other policy tools, including term deposits and term reverse repurchase agreements, if necessary. Most participants thought that the federal funds rate should continue to play a role in the Committee's operating framework and communications during normalization, with many of them indicating a preference for continuing to announce a target range. However, a few participants thought that, given the degree of uncertainty about the effects of the Committee's tools on market rates, it might be preferable to focus on an administered rate in communicating the stance of policy during the normalization period. In addition, participants examined possibilities for changing the calculation of the effective federal funds rate in order to obtain a more robust measure of overnight bank funding rates and to apply lessons from international efforts to develop improved standards for benchmark interest rates.To clarify what is going on here, if the Fed continues to announce policy in terms the fed funds market, this would require that the ON RRP rate be set sufficiently low relative to the IOER so that the fed funds market remains active. Use of the ON RRP facility has some advantages in this context. It works against segmentation in financial markets and thus gives interest-bearing Fed liabilities a broader reach, and it also puts a floor under the fed funds rate. The higher the ON RRP rate relative to the IOER, though, the less fed funds market activity there would be, and the greater the fraction of the interest-bearing Fed liabilities consisting of ON RRPs. Indeed, if the ON RRP rate were equal to the IOER, this might imply that most of the stock of Fed interest-bearing liabilities would be in the form of ON RRPs, as it is less costly for the GSEs and money market funds - which cannot earn interest on reserves - to intermediate ON RRPs than it is for commercial banks to intermediate reserves. Presumably the money market funds would expand and the commercial banks would contract.

2. A large ON RRP facility could eliminate fed funds market activity. Some people might ask why we should care. Borrowing on the fed funds market is unsecured, so each fed funds contract reflects idiosyncratic risk. In general, the "fed funds rate" is not a rate - it's a distribution. And in times of financial stress, the dispersion in that distribution can be substantial. You can see that in Figure 3 of this paper by Afonso et al. To get some idea of how risky the average fed funds market trade is, consider the margin between the fed funds rate and the 1-month T-bill rate in the next chart:

In addition to the fact that the fed funds market is risky, a second problem is that the measured effective fed funds rate does not include all fed funds market trade, but only exchange through brokers. A large fraction of fed funds market activity is over-the-counter, and therefore goes unmeasured. There are indirect ways of measuring activity on the fed funds market, but these are problematic.

A third problem with the fed funds market is that central bank intervention in this market is unwieldy. In pre-financial crisis times, the New York Fed would attempt to hit a given fed funds rate target by predicting, on a given day, the demand for reserves, and then supplying the quantity of reserves that would satisfy demand at the target interest rate. This has lead to substantial fluctuations in the effective fed funds rate around the target, particularly during times of high financial market volatility. During the financial crisis, in addition to the problem that the fed funds rate was a questionable measure of the tightness of monetary policy (due to risk), the New York Fed seems to have had significant difficulty hitting the target.

All of these problems highlight the advantages of the ON RRP facility, and of the ON RRP rate as a permanent target for the FOMC. ON RRP activity is secured, so the ON RRP rate is essentially risk-free, and hitting a given ON RRP rate target is trivial using fixed-rate full-allotment. The Fed would simply fix a rate, and then accommodate forthcoming demand at that rate.

3. A dual system, with IOER above the ON RRP rate, would be more costly than it needs to be. Because holding interest-bearing Fed liabilities is more costly for domestic commercial banks than for foreign owned banks, GSEs, and money market funds, the Fed has to pay a premium to get banks to hold reserves. Thus, the Fed could achieve a given level of monetary accommodation, at lower cost, if the IOER is equal to the RRP rate, than if there were no ON RRP facility. This is roughly what Jeremy Stein is getting at:

You’re saving the taxpayer a little bit of money. You might say one job you give to the Fed is to fund its balance sheet as cheaply as possible.

4. A large ON RRP facility could make the financial system less stable. Sheila Bair, for example, has argued that a fixed rate full allotment ON RRP facility would create a kind of escape route for the liability-holders of financial intermediaries to run to in the event of perceived financial distress.

Even a relatively minor market event could encourage a massive flow of funds to the Fed while contributing to a flow away from other short-term borrowers.Students of money and banking history might find that argument curious. To quote from the original Federal Reserve Act, Congress wanted to

... provide for the establishment of Federal reserve banks, to furnish an elastic currency, to afford means of rediscounting commercial paper, to establish a more effective supervision of banking in the United States, and for other purposes.The idea behind "furnishing an elastic currency" was to provide an escape route. The recurrent banking panics during the National Banking era (1863-1913) were essentially shortages of retail media of exchange. The ability of the banking system to supply media of exchange was impaired during panics, and this disrupted payments and aggregate economic activity. Unfortunately, the National banking system was not designed to take up the slack. With the Federal Reserve System in place, however, the Fed could act to make up for the financial disruption during a panic by supplying more currency, either through discount window lending or open market purchases. Disruption associated with repo runs is not so different. Repos are liquid assets - media of exchange - which are provided by private financial intermediaries. In times of financial stress, as during the recent financial crisis, the repo market can be disrupted. In such circumstances, it is the job of the central bank to take up the slack. One way to do this would be through a ON RRP facility. The private sector could be having a difficult time finding liquid assets, and the Fed could supply them through the ON RRP facility.

So, in conclusion, the ON RRP facility seems neither mysterious nor scary, and could play an important role in U.S. monetary policy in the future.

Thanks for the reply, a whole post nevertheless! :)

ReplyDeleteSo given the availability of these reverse repos,and given that a positive ON RRP rate is set, should we expect the interest on T-Bills to rise due to arbitrage? Or are these RRPs and T-Bills not close substitutes?

Given the IOER, if the ON RRP facility was added, and it was used, that should increase the T-bill rate.

DeleteGood post, Steve. What reasons were given for not allowing GSEs to earn interest on reserves?

ReplyDeleteI don't know. Possibly no one asked, and no reasons were given.

DeleteThis is interesting, but the FOMC has clearly laid out it plans to return its balance sheet to a normal size. This would make all of this moot, no?

ReplyDeleteNo comment, except to say this is far from moot.

DeleteFrom the act authorizing the Fed to pay interest on reserves:

ReplyDelete"Balances maintained at a Federal

Reserve bank by or on behalf of a depository institution

may receive earnings to be paid by the Federal Reserve

bank at least once each calendar quarter, ***at a rate or

rates not to exceed the general level of short-term interest

rates.***"

Paying above-market interest rates on reserves as the Fed has been doing since 2008 isn't just a waste of public funds of around $2 billion/year, it's explicitly prohibited (not that Congress has noticed...)

Paying interest on reserves is not "waste." In fact, the standard economic argument is that paying interest on reserves promotes efficiency. In current circumstances, we could argue that the world would not look different if there were zero excess reserves and $2.8 trillion more in T-bills held by the public. In that case, the Treasury would be paying the interest, not the Fed, and it wouldn't make any difference.

DeleteI said that paying ABOVE MARKET interest is a waste. That's obvious, yes? My point was that the waste was explicitly forbidden by Congress. So this RRP facility thing isn't just a good idea, it's required to (belatedly) comply with the law.

Delete"That's obvious, yes?"

DeleteNo. As it's not clear what that means.

The Fed is the most credit worthy borrower. If it's paying more than an ordinary repo, it's with 100% certainty overpaying.

Delete"We can certainly make a case that a central bank should be targeting an essentially risk-free overnight rate. "

ReplyDeleteI think it would be really effective if the fed issued liabs similar in nature to short term treasuries (uncollaterised) through auctions to the open public and the rate on these securities could be the target. Its seems better to target a risk free rate directly than a interbank rate (FFR) indirectly through IOR and RRP. Why does the central bank need to provide collateral to borrow through RRP when fed securities are already risk free? The fed should just issue securities like the treasury (ON, 1 week, 1 month maturity, etc...) and target the rate on that security.

The fed can contract excess reserves through reducing its holding of treasuries.

Other central banks in the world issue tradeable short-term securities - central bank bills. For example, the Swiss National Bank does it, and so does the Peoples' Bank of China. Indeed, the Fed could intervene by issuing such an instrument and targeting the rate on it. No one is proposing that, as far as I know.

DeleteOn the t-bill/ff spread, even 1-month bills incorporate a forward rate expectation which the funds market doesn't, and 2008 was a period when rates were expected to trade lower, moreover, effectiuve ff was generally trading below the ff target in 2H08, which doesn't seem to be a risk spread story. But don't you think there is also a segmentation issue going on here as well? Bills were in fixed supply (at least in the short run) and in risk-off trades non-banks could only access the treasury market, not funds.

ReplyDeleteI would have used a repo rate if I had it, rather than the 1-month T-bill rate. Indeed, some of the blips in the margin between the 1-month T-bill rate and the fed funds rate pre-financial crisis occur shortly before FOMC meetings when the target is expected to go down (or up). But I don't think all of what you're seeing in 2008 is due to expected decreases in the target. In the paper by Alfonso et al., you can see a big increase in the dispersion in fed funds rates. So there appears to have been substantial idiosyncratic risk in the fed funds market during the crisis. Note also that there's a term premium associated with the 1-month T-bill. That works the other way.

DeleteFascinating post! For the longest time I've been searching for at least a mechanical explanation for why IOER > FF.

ReplyDeleteThis all seems excessively complicated and due entirely to a web of piecemeal regulation. I struggle to see the economic value of repos in a world where any institution can hold interest bearing reserves. Is there an economic argument against the Fed issuing only one type of liability (reserves) and giving direct access to anyone (as opposed to just banks and using ON RRP to get around the law)?

This would seem like a big step towards Prof. Cochrane's run free financial system.

Your idea give me a new era about how to learn & write easily essay writing.I think it give new concept about writing a creative essay.Thanks for it share with us.

ReplyDeleteprofessional essay writing service